CryptoAM: Tether Woes, Infrastructure Grows & Jaguar Roars

Thursday, May 2nd

👋🏼 Happy hump day CryptoAM team. We’re back from our compliance induced break and will be on our normal Tues/Thurs schedule tomorrow.

Over the last 2 weeks we’ve seen an increase of over 1000 subscribers! I’d like to welcome you all to the fold. As always, we welcome you to hang out in our Telegram chat!

Three things you need to know:

One: Bitfinex & Tether

Tether, Tether, Tether. Legend has it that if you say Tether five times in a row, the ghost of Mt. Gox will appear in the mirror and take all your Bitcoin…

At the risk of diving too deep into a subject thoroughly discussed, I wanted to write about the latest Tether fiasco and it’s potential implications. Lots of people have tackled this discussion from different viewpoints, so what I would like to do is take a look at a few different angles and attempt to help you draw conclusions on what the future might look like due to these events. Hopefully along the way you find something interesting you hadn’t thought of previously. I’ll be staying away from legal implications as that’s best left to lawyers.

First, an explanation of what happened. As many of you already know, Tether is a stablecoin company domiciled in the British Virgin Islands. Bitfinex is a cryptocurrency exchange also domiciled in the British Virgin Islands. Both Bitfinex and Tether started as separate entities but then sometime between 2015 and 2017 became inextricably linked, a suspicion many in the space had and was finally confirmed by a Bitfinex representative who confirmed the two companies shared a CEO, Jan Ludovicus van der Velde.

As many cryptocurrency companies unfortunately know, banking is difficult and traditional banks generally don’t support companies that transact large volumes of cryptocurrency. Due to this, both Bitfinex and Tether have bounced around banks quite a bit. After losing it’s relationship with both Wells Fargo and HSBC, Bitfinex put out a statement saying that have “solved” their banking issues. As we now know, this was because they contracted with Crypto Capital, a crypto-native payment processor, to act as their bank. Tether on the other hand managed to secure a relationship with Deltec, a Bahamas based bank.

Fun note: in a twist, Bitfinex’s account at HSBC was actually a sub-account of Global Trading Solutions, which was the owner of Crypto Capital (both were run by the same people…who have now been indicted!) So when HSBC terminated the account, they were onto something.

This is where it really starts to go south. According to the AG report:

During November 2018, Tether transferred $625 million held in its account at Deltec to Bitfinex’s account at Deltec. Bitfinex, in turn, caused a total of $625 million to be transferred from Bitfinex’s account at Crypto Capital to Tether’s account at Crypto Capital, through a ledger entry at Crypto Capital crediting Tether’s account in the amount of $625 million and debiting Bitfinex’s account by a corresponding amount. The purpose of this exchange was to allow Bitfinex to address liquidity issues unrelated to tethers.

In or about late December 2018, the Companies and their counsel developed concerns about the availability of some of the funds at Crypto Capital, totaling over $850 million. While Crypto Capital’s principals have represented that the unavailable funds have been seized or otherwise restrained by governmental authorities in Poland, Portugal, and the United States, the Companies grew concerned that Crypto Capital’s principals may be engaged in a fraud.

Oof. That’s no good. So basically what’s happened is that Bitfinex had a bunch of funds locked up (that’s bad). Tether had a bunch of liquid funds (that’s good). Tether gave Bitfinex a bunch of liquid money (that’s bad), and then Bitfinex gave Tether a bunch a locked up money (…that’s really bad). Of course, they didn’t actually give Tether anything other than a claim to the locked up money if it ever gets unlocked.

If you really want to get into the weeds, I’ll note that technically this transaction of $625M was a sub-transaction of a $900M credit line that Tether extended to Bitfinex. Bitfinex in order to secure this credit line, Bitfinex pledged iFinex shares (the holding company of Bitfinex).

Now, according to the participants — this money is theoretically safe. It’s being housed by governments who would never steal the money and will eventually return the money to Tether holders. This is in line with the thoughts of the market, seeing as Tether’s peg is holding steady after an initial drop off.

The recent timeline:

April 25th: The Attorney General of NY State releases a statement claiming that Bitfinex has lost access to $850M due to a third part payment processor (Crypto Capital) getting it’s funds seized and that Tether loaned them money to help them process withdrawals. The statement alleges that Bitfinex was not truthful to it’s customers about the state of it’s capability to withdraw. Many articles come out with drastic headlines such as “Tether insolvent, missing $850M”…

After the press release, Bitcoin drops 1-2%, holds steady, then plummets ~9% after further spread of the news. Bitfinex outflows begin to heat up and the Bitfinex:Coinbase premium spikes from around ~1% to 8%, another telling sign people are running to get their money off Bitfinex. Note the large spike on the April 26th.

April 29th: Rumblings that Bitfinex is looking to host a token sale begin. The target is said to be $1b, indicating they do not expect to gain access to the frozen funds soon.

April 30th: Bitfinex issues a scathing statement accusing the NY-AG of harming investors, and also confirms that Tether is now 74% backed by liquid securities + cash. 26% of Tether’s backing is locked up with Crypto Capital. The market reacts positively to these announcements and Tether continues to climb back to it’s $1 peg.

General thoughts on the matter:

From a markets perspective, it doesn’t seem like the market cares. Right at the moment tether is trading at a .5% discount. Despite Bitcoin’s immediate crash, the price has held up well and is now trading within 4% of the pre-crash price indicating two things (1) the bear market is probably over (2) the market

Bitfinex’s Bitcoin is still trading at a premium and represents an opportunity for those with long time preference. It’s unlikely that these funds will be lost, which means Bitfinex at some point in the future will regain access and offer fiat withdrawals since their balance sheet is only temporarily affected. If you can wait, you can probably make money. Here are the calculations for breakeven based on cost of capital (lending rate) being 6% a year.

This highlights infrastructure problems and the perverse nature of regulation. Due to stringent regulations and high scrutiny, banks cut off cryptocurrency companies. This by definition forces the hand of these companies to use shady solutions since they cannot access the professional operations. QuadrigaCX (the victim of a $200M dollar loss) also struggled to find banking relationships, with contributed to their use of shady platforms. This event should send a message to both regulators and to companies that there exists a gap that needs to be filled.

Tether was in fact backed one to one. It was only when recent issues with Bitfinex cropped up that they became a fractional reserve system. This bullish but also reminds us that we should probably introduce transparency standards for stablecoins, and why they should not be associated with any other business model (Glass Steagall anyone?)

The case for DAI just got that much stronger. Decentralized stablecoins by nature do not contain any of the risks outlined in this summary. While they do contain a host of other risks, those that value transparency will likely begin to migrate to DAI. DAI is now up about 3%, and is back to dollar parity. This may be due to stability fee hikes, but I’m quite sure the Tether situation played a role. You can confirm this by looking at the DAI charts (DAI/USD spikes right after the press release)

{kind=link}

Two: Infrastructure again! ErisX, TD Ameritrade and Etrade

The main Bakkt Competitor ErisX announced the launch of their institutional grade spot trading product on Tuesday. This comes off the heels of speculation on Etrade launching Bitcoin products as well. While ErisX focuses on the institutional side of things, Etrade marks the beginning of true retail access.

Why this matters: While underplayed, these two announcement marks the beginning of true access to the cryptocurrency markets for both institutional players and your average retail trader. For both, ease of access is everything. Etrade already has 5 million users with more than $10B in capital who are comfortable with the platform. ErisX offers institutions a platform which contains all the tools they are most familiar with.

Every step like this makes it easier for money to flow into the cryptocurrency ecosystem, which makes it more likely that the next market bull will be stronger and more pronounced. 2017 has few trusted entry points. 2019 has many more.

As a firm we just signed up to use the ErisX platform, so I’ll report back with more thoughts once I begin using it.

Three: Jaguar Motors tests smart wallet with IOTA Foundation

Never underestimate how volatile altcoins can be in response to news events. Jaguar Motors, the British car manufacturer, announced plans over the weekend that it was trialling ‘smart wallets’ inside its new vehicles. These smart wallets would allow drivers to earn cryptocurrency on the go - being paid for sharing information about traffic jams, and used to automatically pay for tolls and parking.

Jaguar named the IOTA Foundation as a partner to help explore how distributed ledger technology can be used to make and receive payments in its smart wallet. The result? A near 20% jump in the price of MIOTA of course (MIOTA is the token name).

Interesting enough however if you look closely at the official Jaguar video (screenshot below) you’ll see a range of different cryptos listed on the smart wallet - perhaps a sign that IOTA tokens won’t be the only cryptocurrency available to be used.

Source: Jaguar Motors

Smart wallets will be an integral part of autonomous vehicles. Expect to see more car companies continue to explore this technology. For a vehicle to be truly autonomous it needs to be able to make and receive payments in real time. Distributed ledger technology is a natural fit for this given its immutability and lack of reliance on third parties. And why IOTA? A couple reasons:

Focus on connected devices. IOTA has consistently positioned itself as being focused on the ‘machine economy’ and enabling the sharing economy.

Zero-fee and instant transactions. This reduces friction and allows things like tolls to be paid in real time.

Great, but: According to Jaguar there is no timetable for when the technology might be commercially available. Until then the announcement remains a one off - not a definitive sign that there will be a long term business partnership between Jaguar and IOTA. So often in this industry we see announcements of this kind that don’t actually lead to anything tangible in the long term…

Around the Corner

Also in the News:

Ethereum developer framework Truffle spins out from Consensys

Bakkt Acquires Crypto Custodian DACC, Partners With BNY Mellon on Key Storage

Special announcement:

Techstars, the multinational startup accelerator program, is hosting its Demo Day for its inaugural blockchain accelerator program this Wednesday 1st May. The accelerator includes 10 top blockchain startups from the US, Czech Republic, Canada and South Africa.

Want to see what the most cutting edge companies in the space have been doing? Sign up here to have access to an exclusive livestream of the event, which kicks off at 4.45pm EST.

Market Outlook:

Quick Take

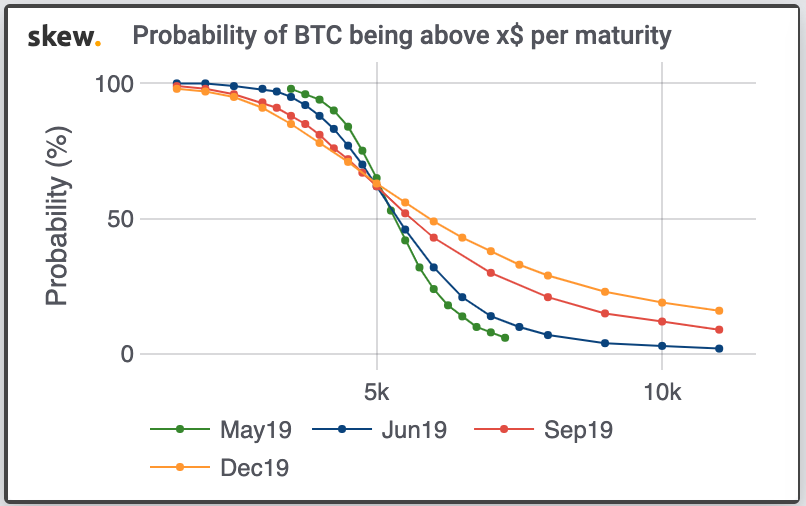

Direction: Bitcoin is looking quite strong after shrugging off the Tether news and climbing back up to the 5300 level. We’re looking at a very weak resistance and strong support, which has me leaning bullish. Volatility is also ticking up nicely, and probability of 10k by December is now sitting at a healthy 20%.

Key Support: 5300

Key Resistance: 5500

What I’m reading today:

The Business of Stablecoins - Aleks Larsen

With all the Tether/Bitfinex controversy, what better time to throwback to one of my favorite articles about stablecoins. The focus here isn’t on how different stablecoins work, but how stablecoin providers actually make money and profit.

A reminder for those who may be more new to the industry: stablecoins are cryptocurrencies with stable values. Ideally they share the features of Bitcoin but they don’t suffer from the same volatility. This makes them more suitable as a store of value, medium of exchange, and unit of account. However no stablecoin has yet been able to fully fulfill this ideal - see here for more context.

Now, onto how stablecoin providers make money:

1) Fiat backed stablecoins

Examples: Gemini Dollar, Tether, TrueUSD

The most common type of stablecoin, fiat backed systems accept fiat currency or non-crypto assets as collateral, store this with third party custodians, and then issue stablecoins in a 1:1, IOU format.

Example: I pay you USD$100, you store that USD$100 with a third party, and then you give me $100 worth of your stablecoin, let’s call it AKL. Now I have $100 AKL tokens that should be worth USD$100 at all times.

How the stablecoin provider makes money:

1. Charging fees on issuance and redemption. Each time I want some of your AKL tokens you charge me a small fee, and you do the same if I want to redeem my AKL tokens for USD. If you assume say a 0.1% fee for either service and $10B of inflows and outflows annually, thats $10M revenue.

2. Short term lending. The stablecoin provider may choose to invest a portion of the funds they have from consumers into short term treasuries and money market funds.

Let’s play this scenario out. TrueUSD has a market capitalization of just over $200M right now. Let’s say they also have a reserve ratio of 50%, meaning that they keep $100M in the bank for customer withdrawals and put $100M into short term treasuries. 1 month US treasuries currently yield 2.4% annually. This would net them $2.4M annually from this strategy.

This is similar to the concept of … a bank. Yes, these types of stablecoins have more in common with your run of the mill bank than they do with cryptocurrencies. Often you’ll see stablecoin issuers take on the role exchange, custodian and more in addition to their role as a stablecoin provider. The real-world analog of this would be banking institutions pre-2008 before banking regulations broke up the trading side of things from the consumer deposit side. It’s up for debate whether that should happen in crypto, but if the recent Tether news is any example…maybe we need a Glass-Steagall for crypto…

3. Market-making. Especially for exchanges that have their own stablecoin (Gemini, Circle etc) they may look to reduce the size of the bid/ask spread on their own exchanges.

Key note: Aleks mentions that centralized exchanges with their own stablecoin may not actually need to monetize them. This is because these exchanges benefit from them in other ways, such as using these stablecoins as an on-boarding tool for new users and as a safety asset. This may put these exchanges at a unique advantage; they can offer lower issuance and redemption fees because there is not as much pressure to directly make money from stablecoin operations.

2) Crypto backed stablecoins

Examples: DAI

This is a more decentralized approach in contrast to fiat backed stablecoins. These types of stablecoins often have a ‘volatile’ coin in addition to the stablecoin. The volatile coin is meant to incentivize behaviors that benefit the system. Take Maker as an example which has:

DAI - the stablecoin which aims to stay pegged 1:1 with USD.

MKR - the ‘Maker’ coin which is volatile.

Why is the volatility coin important? Because it is usually where value accrues in this model. Again, using Maker as an example, let’s look at the ways money might be made:

- Rights to interest on collateral. In the Maker system this is represented by the ‘stability fee’, which is basically the interest rate paid on DAI that has been borrowed. Except this stability fee can only be paid back in MKR tokens, and these tokens are then burned. The important point here is that this decreases the overall supply of MKR tokens. We could expect this then increase the price of MKR tokens, benefiting all MKR token holders.

- Rights to transaction fees. This would include fees on on-chain transactions that are paid proportionally to volatility-coin holders. Value would therefore be derived from transaction fees and also from the fact that as the stablecoin network usage increased, you would assume the price of the volatile coin to increase also because holders are gaining more transaction fees. This has the potential to yield large returns, but is something that hasn’t been implemented successfully yet as far as I can see. It might also hinder usage of the main stablecoin because users would be incurring extra costs for each transaction.

There’s also a third category of stablecoins - algorithmic - which have their own associated business models. It’s unlikely that an algorithmic stablecoin will gain a foothold anytime soon due to numerous economic problems that would require incredibly complex mechanics AND a very trusting population to solve. Major projects such as Basis have already tried and failed (despite raising $133M!)

It’s a complex and largely theoretical field currently but if you’re interested, I encourage you to check out the original article and read into it more.

Join the conversation on Telegram and Twitter

If you ❤️ our newsletter, tell your friends about us!

Nothing written in CryptoAM is legal or investment advice and should not be taken as such. CryptoAM does not make any guarantee or other promise as to any results that may be obtained from using our content. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence.