CryptoAM: Securities Law, a Brave New World, and JPM thoughts

Tuesday, March 12

3 things you need to know:

One: SEC Chair (kind of) Implies that Ethereum is Not a Security

Yesterday, the Chairman of the SEC affirmed that he agreed with SEC Director Hinman’s prior analysis that it’s possible for a cryptocurrency to go from being a security to not. What it legally becomes at that point is unclear, but it’s more likely than not that it becomes classified as a commodity.

The money quote:

“I agree with Director Hinman’s explanation of how a digital asset transaction may no longer represent an investment contract if, for example, purchasers would no longer reasonably expect a person or group to carry out the essential managerial or entrepreneurial efforts. Under those circumstances, the digital asset may not represent an investment contract under the Howey framework.”

…“No one is creating it for their own … control of bitcoin, it’s designed to be a payment system replacement for sovereign currencies. We’ve determined that that doesn’t have the attributes of a security … as far as I’m concerned, that’s designed to be akin to the dollar, the yen, the euro … and it operates that way. People who purchase it are expecting it to operate that way.”

There are unfortunately many lingering questions. Technically there are “groups” of people that maintain Bitcoin and Ethereum. If a group messes up and implements bad code, the project would lose value. It just so happens that the group is massive and ever changing. Where do you draw the line between the two?

The other statements betray the lack of understanding in the regulatory world of the makeup of Bitcoin enthusiasts. The vast majority of people definitely do not expect Bitcoin to act as a euro, yen, or even a dollar. They expect it to act as an early stage investment and to deliver high returns. Bitcoin is also highly decentralized. So where does that land? Ultimately, I believe that we’re going to need different securities laws than the Howey test.

It’s also interesting to me that the SEC and CFTC commissioners have suddenly become rockstars in the world of crypto, and are now appearing at many different conferences around the country to share their views — in no other industry are regulators so sought after and given such stage time. Despite Elon Musks best efforts to drag down the (S)hortseller (E)nrichment (C)ommission, the commission and its counterpart the CFTC seem to be massively growing in popularity in the cryptocurrency world. Chris Giancarlo (CFTC) and Hester Pierce (SEC) are showered with praise on a daily basis! What a weird world we’re living in.

Two: Brave browser enters phase two as downloads surge past 20 million

The Brave internet browser, which looks to reward users with its Basic Attention Token (BAT), announced over the weekend that it had entered phase two of its Brave Ads Developer Channel Preview. Phase one never actually involved giving users BAT for viewing ads, instead being a trial period for stakeholders to test the browser. Phase two involves users actually being compensated with BAT for opting in to view ads.

Users will be compensated with 70% of all ad revenues that are generated. The other 30% will be split evenly between publishers (websites that host the ads) and between Brave browser itself. How much revenue this generates is yet to be seen, especially as advertisers so far have primarily been crypto companies.

Why this is important: Lack of adoption is crypto's Achilles heel. Brave browser however has been downloaded over 20 million times and has been in the top 1% of all android app store downloads. This is with a product that is avidly privacy focused - imagine what it would be like to be compensated for every ad you viewed on Chrome or Safari?

Three: Kakao raises $90 million for new blockchain in private coin offering

South Korea's main messaging app Kakao announced Monday that it had raised $90 million in a private coin offering. The company also plans on raising an additional round of the same amount as it prepares to launch its own blockchain platform in June. The platform's name will be Klaytn.

26 companies are signed up to run their applications on the new platform. While a wide range of services will be offered gaming apps are seen as particularly promising.

How they were able to raise the money legally: According to Cointelegraph, the tokens were only made available to registered and pre-vetted investors. The company's blockchain subsidiary, Ground X, is also based out of Japan. This allowed it to circumvent the increasingly strict regulation coming out of South Korea.

Unlike other messaging services like Telegram and Signal, Kakao hasn't yet confirmed that it will bring its messaging service onto the platform. Messaging apps launching their own token have been the subject of intense interest recently, particularly in the case of Facebook and Telegram that are expected to launch tokens later this year.

Remittances, remittances, remittances. The value of integrating a token with messaging applications is explored below, and also briefly in the previous sentence.

Also in the news:

Wash trading continues at large crypto exchanges (Will have thoughts about this on Thursday…)

Alan Howard’s Elwood Targets Big Investors for Digital Assets

Market Outlook:

Quick Take

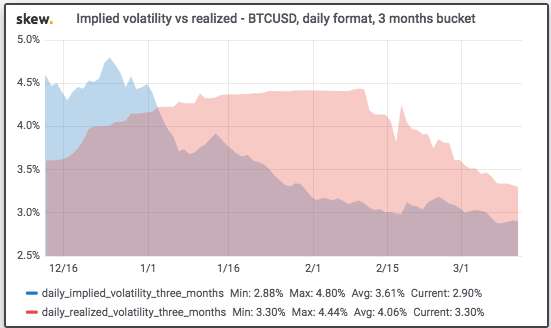

Direction: Bitcoin has stabilized over the last week, trading in the range of 3850 (previous resistance) and 3900. Based on overall past movement, there seems to be strong support at these price levels and the market is indicating Bitcoin is fairly valued around the 3500-4000 level for now. Looking at transaction volumes, we’ve seen a steady increase to early 2018 levels despite a decrease in price, telling me that Bitcoin is becoming *more* fairly valued based on network value to transactions ratio.

Both implied volatility & realized volatility are trending down, which indicates the next move will be explosive rather than a slow melt up/down. The gulf between implied volatility & realized, while narrowing, is still indicating it’s a good time to buy long term volatility.

I personally am not taking directional trades here because I view most price action in this range as noise, anyway. I’m more comfortable taking bets on volatility, and bets on the decline of BTC dominance as generally periods of stability lead investors to pile into “undervalued” alt-coins.

Key Support: 3730

Key Resistance: 3850

Fear & Greed

F&G agrees with technicals, and suggests it’s more like that we experience a run up than down.

Here’s a reminder of what these criteria mean

What I’m thinking today:

Some thoughts on JPM Coin, Bitcoin, Ripple & the Future.

As you may or not know, JPMorgan has a coin now. They introduced it about a month ago to much fanfare and cries from the general public that this announcement was the beginning of the institutional wave. (Note, they are definitely not coming in for JPMcoin, but ok).

For the may nots, here’s a link.

Now the feasibility and use of this coin depends on your point of view. If you’re JPMorgan, you’re probably very excited about launching a blockchain product. It’s nifty, it’s cool and now people are looking to you as a leader not just in credit card bonuses but also in blockchain technology. JPMorgan (to their credit) actually has an incredibly strong tech team, and their own implementation of Ethereum (called Quorum) is a really interesting application.

Going back to the coin, it’s function is to be a stable-coin within the walls of JPMorgan and improve transaction efficiency by losing less money when moved around. I imagined this conversation:

Jamie: “We need to improve. It takes way to long to move money around”

Engineer: “Well, we could copy Bitcoin, or Ethereum. They seem to be decent settlement layers.”

Jamie:

Engineer: “How about we use blockchain instead?”

Jamie: “Sounds great.”

If you’re building a financial system, you want three things. (1) you would like things to be neat and function efficiently (2) you want a lot of people to be able to access your system (3) you want to make sure things don’t blow up too much.

Now JPMcoin seems to address (1) & (3) pretty well, as money will probably move faster within the system but (2) poses an issue.

You have to think to yourself why Citibank, Bank of America or any other institution that would greatly benefit from their own coin actually use JPMcoin? The answer is they aren’t going to. While JPMcoin may work neatly within the confines of it’s walled garden, it probably isn’t going to be adopted by the broader financial system any time soon.

This is where third parties like Ripple have an advantage. Ripple succeeds at (1) & (2) but not necessarily (3), as people are skeptical that the whole thing won’t just blow up one day for a myriad of reasons.

This is not to say all “institutional” stablecoins are doomed to fail. It’s just hard to imagine adoption of a JPMcoin in a place where regulations and risk-averse managers are abound. Can you imagine Johnson&Johnson doing a transaction with JPMcoin and accepting the coin as settlement? They wouldn’t want to lock themselves into the system, and they aren’t going to go to a BoA right after and expect them to accept JPM.

A Facebook coin has a much better angle of attack. Starting with their massive base of consumers, they can issue coins that in the beginning with mainly be used for p2p transactions. Slowly people stockpile these coins in their “accounts” and will eventually require usage for them and will tire of constantly cashing out. For example, you can now use Venmo to pay for Uber, because a ton of people have Venmo balances and wanted to do something with it. With monetary adoption, starting with the individual is a lot easier than starting with an institution.

The last point about this is a little bit more philosophical in nature. This stablecoin, along with most other 1–1 fiat collateralized stable coins is not really a cryptocurrency in any meaningful way. It may use blockchain technology, but it’s most definitely not a cryptocurrency. I believe people tend to get mixed up between the two, and in a deeper way than most people tend to think.

This application of JPMcoin is not the issuance of a new cryptocurrency, but rather the moving of the JPM ledger to a blockchain. The “coin” part is meant to confuse and move you away from realizing that this is just a back office efficiency, a way of tracking movements a little better. They’ve upgraded their database, not switched to a new currency.

The wonders of branding though made it seem as though a new currency was hitting the market.

Join the conversation on Telegram and Twitter

If you ❤️ our newsletter, tell your friends about us!

Nothing written in CryptoAM is legal, or investment advice and should not be taken as such. CryptoAM does not make any guarantee or other promise as to any results that may be obtained from using our content. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence.