CryptoAM: Poloniex, Synthetic Assets & Facebook

CryptoAM: Poloniex, Synthetic Assets & Facebook

Another day another full-on crypto news cycle. Lucky you’ve got two very part-time “journalists” to keep you informed 🔥

Three things you need to know:

One: Poloniex loses 1800 BTC because of a CLAMS flash crash

Flash crashes are a common occurrence in the cryptocurrency markets, and happen with regularity on both liquid and illiquid pairs. Some of the most famous flash crashes in history have seen price drop tremendously.

Those of you around in June ‘17 remember the famous Coinbase flash crash, where Ethereum dropped from ~$300 to $0.10 in a matter of seconds, liquidating many people on the way down. This crash led to Coinbase disabling their margin trading feature and then reimbursing margin traders to the tune of $10M.

Well, it’s happened again, but this time on Poloniex with a relatively illiquid coin called clams (CLAM). On May 26th, a large crash in the CLAMS market forced liquidations of many borrowers who had posted collateral in CLAMS. Due to the speed of the crash, many of the borrowers went negative collateral-wise, and therefore sustained losses they were not able to repay and sustained losses of 1800 BTC.

From the Poloniex statement:

The losses to the lending pool occurred for several reasons. First, the velocity of the crash and the lack of liquidity in the CLAM market made it impossible for all of the automatic liquidations of CLAM margin positions to process as they normally would in a liquid market. In addition, a significant amount of the total loan value was collateralized in CLAM, so both the borrowers’ positions and their collateral lost most of their value simultaneously. As a result, some borrowers were unable to repay their loans with the digital assets they held on Poloniex.

In response to the 1800 BTC deficit, Poloniex socialized the losses among margin lenders who will now be taking a 16.202% haircut on their principle (!)

This highlights a major issue in the cryptocurrency lending market that people seem to gloss over — margin requirements and correlation. If you are able to borrow asset A by posting collateral in asset A, you’re exposing yourself to double risk, and margin requirements should be adjusted to reflect this (on Poloniex, they were not).

Go deeper: Read the Poloniex statement

Two: The emerging world of synthetic products

Decentralized finance has taken the cryptocurrency world by storm over the last few months, with many new protocols breaking onto the scene. The vast majority of DeFi protocols currently focus on providing decentralized leverage and lending, and are all quite similar to each other but with different UI, UX, and lending rates.

More recently, a differentiated crop of DeFi protocols have appeared, focusing on the creation and proliferation of synthetic assets. Below I highlight a few interesting approaches to synthetic assets:

UMA Protocol: UMA is the first decentralized protocol I came across that offers synthetic instruments, and does so in an interesting way (albeit flawed in edge cases). The basic premise is that two people enter into a contract for *any asset* with one going long and the other going short.

Both people post a certain amount of collateral to that smart contract and based on the way the position moves, they are required to post additional collateral to the smart contract to avoid liquidation.

There is a fee associated with the collateral that is exercised if the position moves against you and you don’t post additional collateral. This theoretically incentivizes people to add collateral so that they have a shot of retaining their full position if the underlying asset begins moving in their favor again.

This obviously falls apart if one counter-party’s view on the asset changes and they believe it’s now heading in the opposite direction of their initial trades, but is still probably good enough for low volume assets.

Synthetix: Synthetix is a nutty protocol that is already up and running, offering a multitude of both synthetic cryptocurrencies and stocks.

Synthetix has a token (SNX) associated with the system, and requires users to stake SNX as collateral in order to create “Synths”. Staking SNX entitles you to a portion of the fees that the network generates and allows you to mint their synthetic stablecoin, which you can trade on their DEX for other synths (this is where the fees come from)

Each “Synth” has its own smart contract associated with it, unlike UMA which has separate smart contracts for each trade.

Abra: While not decentralized, I believe that Abra deserves a mention here for their pioneering work on synthetic assets.

I spent a long time trying to understand their infrastructure, which they outline in a series of great posts. Abra seemingly offers exposure to a multitude of different assets on their platform, but in reality there are only three assets that Abra truly holds the real, non-synthetic version of: Bitcoin, Litecoin and Ethereum. The rest of the assets are all synthetically created using smart contracts and Abra’s trading desk. Abra offers both cryptocurrencies and traditional equities on their platform, and is a great bet for those more comfortable with centralized solutions. I mean, where else can you punt stocks with Bitcoin?

Three: The Financial Stability Board report on decentralized technologies

The Financial Stability Board released a report yesterday on the effects of decentralized technologies and their potential problems. Some choice quotes:

If tokenisation were adopted more broadly, it is possible that it might create an appearance of liquidity in assets that are inherently illiquid. This may also have negative implications for financial stability. In particular, risks could arise where there is a liquidity mismatch between the token and the underlying asset, or where investors have limited understanding of products packaged into a token. For example, the tokenisation of real estate (were it to become widespread over a large geographic area) might threaten investor confidence in certain areas were investors to overestimate the degree to which the underlying assets could be sold at (or close to) prevailing market prices during periods of stress.

Basically, the FSB thinks that the tokenization of assets could drive investors to overestimate liquidity and enter into positions that may seem more liquid than they actually are. What the report fails to point out is that a world with tokens does introduce more liquidity than a world without tokens. The report insinuates that an investor may be lulled into a false sense of security, but that is true with a variety of financial instruments that currently exist on the market…

Some better points below:

It is important that regulators continue to assess the degree to which current rules provide adequate safeguards in the case of tokenisation. Issuers of tokenised securities should also properly consider applicable regulation. This could include issues around: (i) settlement and settlement finality and the role of miners and validating nodes (which may fall outside of existing regulations); (ii)the safekeeping of private keys and the interactions with the existing custody/safekeeping rules; and (iii) the security of the underlying DLT protocol and codes, including in relation to smart contracts. To the extent that tokenisation widens the potential investor base for a variety of products, effective application of investor protection rules may similarly require careful consideration.

&

The shift towards smart contracts and self-executing code could also create specific governance and accountability issues. These include the question of whether – and to what extent – software developers, system operators or users can be held responsible if contracts do not function as intended.

Go deeper: Read the full report

Also in the news:

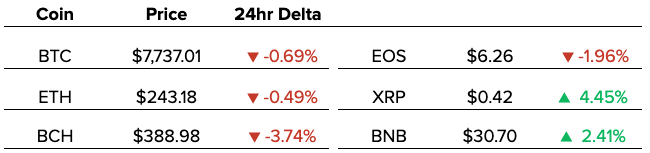

Market Outlook:

Quick Take

Direction: We’re still in a similar market structure to Tuesday’s structure. It looks short term bearish but I’d expect some dead cat bounces until then. I believe Bitcoin is far more likely to revisit 7k than 9k, and still more likely from here to end below 7200 than above 8000 by the end of next week.

Volumes have been dropping off, as have on-chain transactions. Many of the buyers who would have entered the market are already in. Something to note is that altcoins are still holding up well, and we may be seeing some flows from BTC profit taking into alts.

Key Support: 7600

Key Resistance: 7800

Overall Market: LEO is outpacing the market significantly, and it’s likely the first buyback has already started. Combined with the upcoming IEO on the Tokinex platform and more announcements rumored to come, I believe LEO is a in a good position to outperform. As a disclosure, I already have a position here. As for other alts, I’m looking to enter platform coins that with upcoming releases that have bottomed. Now is a good time to enter into your favorite alt positions…

What I’m thinking today:

What we know so far about Facebook’s GlobalCoin

After months of speculation throughout the cryptoverse, yesterday details were revealed about how Facebook is attempting to structure its GlobalCoin. The whitepaper launch is set for June 18th (viewing parties strongly encouraged).

If you had any doubts about how seriously Zuck is taking this project, here’s an excerpt from The Information’s report:

“When the team behind the Libra project initially presented their plans to Mr. Zuckerberg, it discussed three possible investment scenarios the company could make in the effort - low, medium and high - and the Facebook CEO chose high.”

Here are the four key things to know about it:

Governance

An independent foundation will be created separate from Facebook to govern how the Coin operates. Facebook has apparently courted financial institutions and tech companies to be a part of this.

Reason: Keep the regulators away. Antitrust investigations on Facebook are beginning to heat up independent of GlobalCoin, meaning that the company might be trying to avoid throwing gas on a fire.

Our thought bubble: This is basically the same concept that cryptocurrencies like Ethereum, Cardano and Tezos have employed. How independent these and other crypto project’s foundations actually are is an open question however. You can expect much more in-depth scrutiny of Facebook’s foundation.

Regulatory Compliance

Facebook has been working closely with multiple governments to get the token approved and plans to provide more stringent forms of identity verification and fraud detection.

Reason: Anti-money laundering and KYC laws are a giant problem for any financial institution. If Facebook wants to have responsibility for the movement of large sums of money within its system you can bet it’ll have strict policies in place to make sure it complies with local regulations.

That’s likely to be anathema to those who are concerned about privacy (Facebook doesn’t have a stellar track record here). It’s also likely to add friction to the onboarding process for customers who will have to verify their identities before being able to purchase GlobalCoin.

Another potential consequence of this is that people without formal identification miss out. There’s 1 billion of these people in the world. That being said, Facebook probably has a drove of data on these people via their Facebook accounts, and so it’ll be interesting to see whether they can leverage this with governments to lower barriers for these people to use GlobalCoin.

Validating Transactions

Facebook is looking to charge external parties…

Wait for it…

$10 million to run a node for the GlobalCoin network. It hopes to have at least 100 of these. To put this into context the Bitcoin network has close to findable 10,000 nodes while Ethereum has around 6,500. The big difference obviously is that with Bitcoin and Ethereum to add a node you don’t need to pay anyone, it’s completely open to all.

It clearly won’t be as decentralized but the key question is: Do regular users care?

Encouraging Adoption

Facebook will offer sign-up bonuses to users via partnerships with merchants. These merchants will accept GlobalCoin as a method of payment in stores.

There isn’t currently an indication of whether there will be big name merchants included in this, or whether merchants will have to adjust their existing payment rails to accept GlobalCoin. A big question here is whether Facebook or a partner payment processor converts the customer’s GlobalCoin into fiat for the merchant at the point of sale or whether these merchants will accept and hold GlobalCoin itself.

Predicting the future is a total fool’s errand. That’s why I’m going to do it anyway. Here’s some final thoughts:

GlobalCoin will have its own blockchain. They’re setting up their own foundation, and charging people to become nodes on the network. I can’t see anyway you’d be able to do that while building on-top of another blockchain.

Size matters here, especially for those merchant partnerships and potential discounts for consumers. Let’s say Facebook works out an agreement with merchants where consumers get a 5% discount if they use GlobalCoin. Facebook can take the hit on this if, for example, they give partner merchants 5% off all ad purchases on either Facebook or Instagram. The key here is they have the resources to be able to take the short-term revenue hit to boost adoption. This is also important to help consumers get past the friction of initial AML/KYC onboarding.

How will nodes earn revenue to compensate for the $10 million they’re spending? There won’t be any transaction fees according to the company. My guess here is that nodes function as miners, and gain benefits from block rewards although this could be way off.

How much money Facebook makes on this is still unclear. I’m guessing some revenue comes from interest on fiat-deposits as well as the potential for issuance and redemption fees.

As mentioned in the report, developing countries with volatile currencies are going to be the focus for this launch. I’d be looking closely at countries like Argentina, Turkey, India and Egypt. I continue to believe that helping poorer individuals in these countries to access a stable store of value could bring Facebook some much needed good PR.

Join the conversation on Telegram and Twitter

If you ❤️ our newsletter, tell your friends about us!

Nothing written in CryptoAM is legal or investment advice and should not be taken as such. CryptoAM does not make any guarantee or other promise as to any results that may be obtained from using our content. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence.