CryptoAM: Libra, MetLife, Algorand, and the Markets

Happy Friday, CryptoAM crew! We’re heading into this weekend with glee, looking at these Bitcoin prices. We’re encroaching on $10,000. Hold on to your hats.

Three things you need to know:

One: Why Libra actually matters

We've both thought long and hard about Libra and what it means for people. Whether you like it or not, it's something that (if it launches) will transform our industry. Here's our honest take on what we believe is important:

1. A new wave of people are about to enter crypto. Facebook has a reach of 2.7 billion users. Imagine just 1%, or 27M, of these people go down the crypto rabbithole, exploring other currencies and choosing to develop on top of the Libra infrastructure. Depending on your figures, that's anywhere from a 30% to 70% increase in people interacting with crypto.

An important step before investment is familiarity with an investment. Most people have heard about stocks, bonds, real estate, gold, etc. The list of traditional investments goes on, and the majority of investors have at least passing knowledge and some comfort in these instruments. Facebook’s cryptocurrency will introduce the concept of a non-governmental currency, which may entice people to be more comfortable checking out other forms, such as Bitcoin.

Libra may also have a negative affect on Bitcoin adoption, as it expands to countries that have weaker currencies. One major value proposition of Bitcoin is that it allows investors to hedge against the demise of their own currency. For countries with already weak currencies, the Libra will present an enticing alternative for this hedge as it will be easily accessible and usable. Of course, countries whose currencies make up the reserve basket of Libra will not be able to benefit as much, but they are likely to be stable countries and less in need of such hedges.

2. This is a significant challenge to the traditional financial system. Retail banks and central banks will be in the firing line, and the overall implications of this are unclear. Consumers in countries with weak currencies will have easier access to a stable store of value. On this point it’s important to highlight the difficulties of dollarization, where countries have adopted the US dollar (Ecuador, Panama) and now have no control over their monetary policy and have less ability to respond to recessions. It’s possible we see something similar if Libra gains traction in these countries.

If the Libra accumulates large amounts of assets, it will have the ability to impact the global economy and foreign exchange rates (as it will be a large buyer and seller of a variety of currencies). This makes Libra an inherently political organization and economic weapon. Expect governments around the world to request a seat at the table, and the evolution of Libra into a pseudo-central bank is not unlikely if successful.

Why this matters: It affects the lives of literally millions of people. Expect to see increased discussion about monetary policy, who should have control over it, and what optimal policy looks like. Is the monetary policy of Bitcoin suitable for entire countries? Is Libra? See here for a great discussion on this issue.

3. Privacy and decentralization remain important issues. The Head of Libra, David Marcus, has stated that neither Facebook, nor the validator nodes, will have access to any financial transaction information that goes through the Calibra digital wallet. However his answer about whether Calibra itself will use the data was more ambiguous, although users would have the opportunity to use other other wallet providers if they had concerns.

4. The goal is to become permissionless in five years. The importance of this is that any node could join and leave the network without friction, which decentralizes the overall network. The reason for this is sustainability; it’s not feasible for the same 27 organizations to run nodes for hundreds of years, especially as business fortunes change.

Here’s another way to think about that $10 million investment that validators are currently required to pay, as per David Marcus himself:

“If we end up in a proof of stake consensus algorithm…the entities that will have invested the most, that will have the most impact on this ecosystem, will have an equivalent governance.”

A couple key questions for you the reader:

- From a privacy standpoint would you prefer to use Libra or the Chinese Renminbi on WeChat or AliPay?

- If Libra became permissionless over time and had 10,000 nodes (similar amount to Bitcoin), would you consider that sufficient decentralization?

Finally, consider this more lighthearted thought:

Do you really think Zuckerberg accidentally named this Libra while the Winklevoss twins have a company coincidentally called Gemini?

Two: MetLife looks to reinvigorate life insurance industry

MetLife, the $47 billion life insurance giant, has announced a 1000 person blockchain pilot program in Singapore for June 2019 to add transparency and efficiency to the claims process. The technology is called Lifechain (I'm not joking), and will be built on top of Ethereum. The pilot is the first in the world focused on the life insurance industry.

The problem they're solving: When someone passes away there are usually 101 different things that need to be done and organized. Filling out a claim for the decreased person's life insurance - assuming the family even knows that person had insurance - often falls down the priority list. Imagine it another way: You probably don't want to spend time trying to find out if your loved one had life insurance, and then have to fill out a redemption form, while you're in the middle of grieving.

The approach: A common step after someone passes away is to report a death to the newspaper for the obituaries. This is where the process begins, as Singapore Press Holdings (who owns the newspapers) uses the death certificate from the obituary and works alongside LumenLab (runs the LifeChain tech) and NTUC Income (an insurance cooperative) to automatically validate whether the deceased person had a policy. If a match is found, then the appropriate beneficiaries are contacted.

Think about that for a second. You report your loved one’s death to the local newspaper. Without needing to do anything further, if the deceased had life insurance the insurance company gets in contact with the policy-nominated beneficiary. You’ve removed the need to contact a life insurance company; they get in contact with you.

The limitations: Ethereum can handle a 1000 person pilot but without upgrades would likely face problems if the industry ended up adopting a similar system. The CIO of MetLife Asia, Zia Zaman, mentioned this issue in Forbes and stated that the company may look at other blockchains in the future.

Why it matters: Set dates, clear success criteria and a decent pilot size. These are all the things that tend to go missing whenever we see announcements of big companies exploring blockchain or, even better, when these companies announce 'partnerships' with blockchain companies.

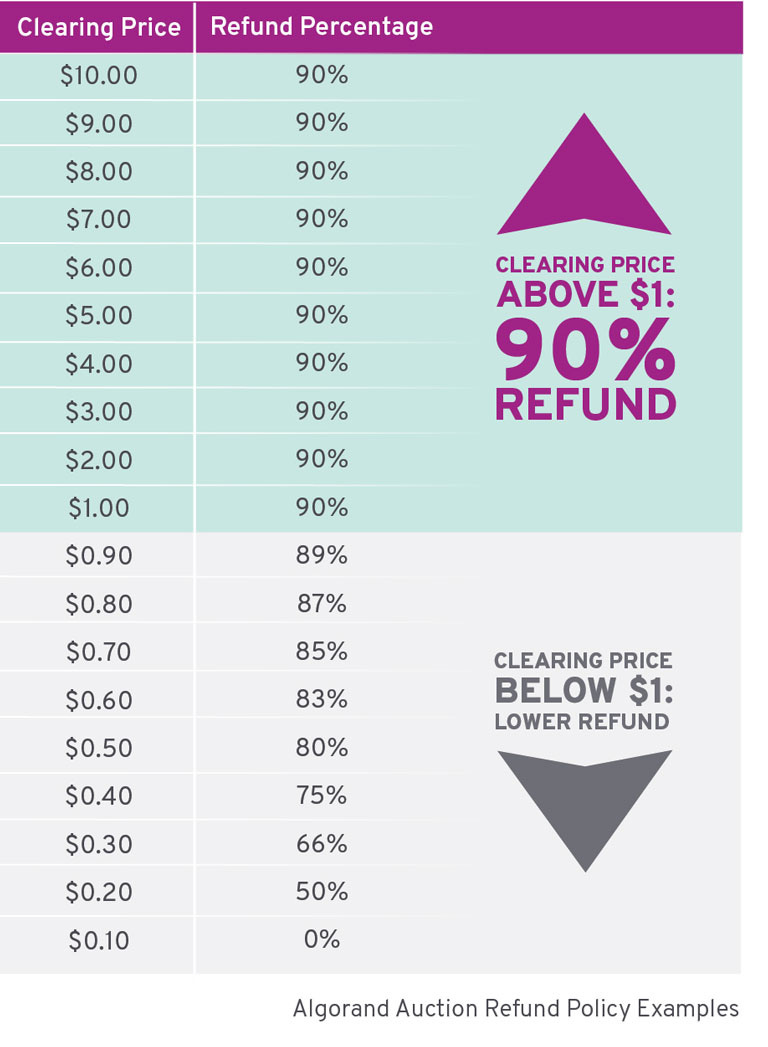

Three: Algorand raised $60M (or $6M?) in their first Dutch Auction

Algorand, one of the most high profile launches of 2019, just finished its first token auction. Algorand sold 25M tokens at $2.40 each, for a total of $60M. The pricing on the first round of tokens implies a fully diluted valuation of $24B, which would place Algorand right under Ethereum ($31B) in total market cap rankings(!!).

Even more surprising, Algorand is now trading above the initial offering price — $3.12 at the time of writing — placing its market capitalization right on par with Ethereum.

Algorand’s auction was a first for the cryptocurrency markets as participants in the auction were promised a certain % of their investment back as a refund, based on the clearing price of the dutch action (explained here). This means that in reality Algorand raised $6M in operating capital, and must save $54M for a year in a segregated account in order to ensure they have the money to refund initial investors.

Algorand has effectively given investors a put option, limiting their downside and allowing investors to take on more aggressive positioning. This also introduces major incentive on behalf of Algorand to ensure the price of their token remains above the average price of auctions. This may prove to be a difficult feat, as Algorand has garnered a massive valuation despite only launching mainnet 2 days ago, in conjunction with the auction.

Why this matters: Algorand is undoubtedly the biggest cryptocurrency to hit the scene since EOS launched in 2018. It will be one worth paying attention to over the coming months, especially as the protocol begins to attract applications and developers. For those looking to learn more, both the Arrington XRP Capital and Binance Research have released stellar reports.

Also in the news:

Market Outlook:

Quick Take

Direction: Bitcoin continues pushing up towards 10k, getting as high as 9962 (Bitstamp) this morning. There have been slight pullbacks but the bull trend is still very much so intact.

Bitfinex longs have increased at a strong clip over the last week, but are still far from their March peaks, and BitMEX funding rates are actually trending down despite continued price appreciation, indicating that this rally is not as highly levered as previous rallies and that there is likely still appreciation to come.

Chart above courtesy of Joe McCann, who has a great markets letter

Futures are also trading with a nice forward curve, implying the market has a bullish bias. Options across the board on Deribit are implies probabilities of > 51% that we end their given expiry above 10k.

We are now in the second parabolic advance of this bull market (as displayed in the chart above), which generally end in strong corrections (30%). The key level to watch here is of course, 10,000. There is a significant amount of sell pressure at those levels, but I expect a lot of sell pressure to evaporate as 10k is breached as people will be expecting further appreciation.

The two major scenarios in mind are a full on break of 10,000 at which point we probably trade up another 8-10% to 11000 shortly, or a strong rejection which signals the end of the parabola, and a price drop to the 8800 level.

My personal bets are long volatility with a small upside bias. I believe that regardless of where we go from here, the moves will be violent and have bought calls and a smaller amount of puts to reflect my predictions. I retain that upside bias, and place a 75% chance on breaking above 10k and going to 11k and a 25% change of retracement.

Key Support: 9800 (weak), 9300 (stronger)

Key Resistance: 10,000 (strong)

Overall Market: During this run, Bitcoin has posted continued BTC dominance gains, and I expect that to continue if Bitcoin manages to break 10k. A pullback from the 10k level would give altcoins room to rally, but until then being weighted towards Bitcoin is likely an EV+ move.

What I’m thinking today:

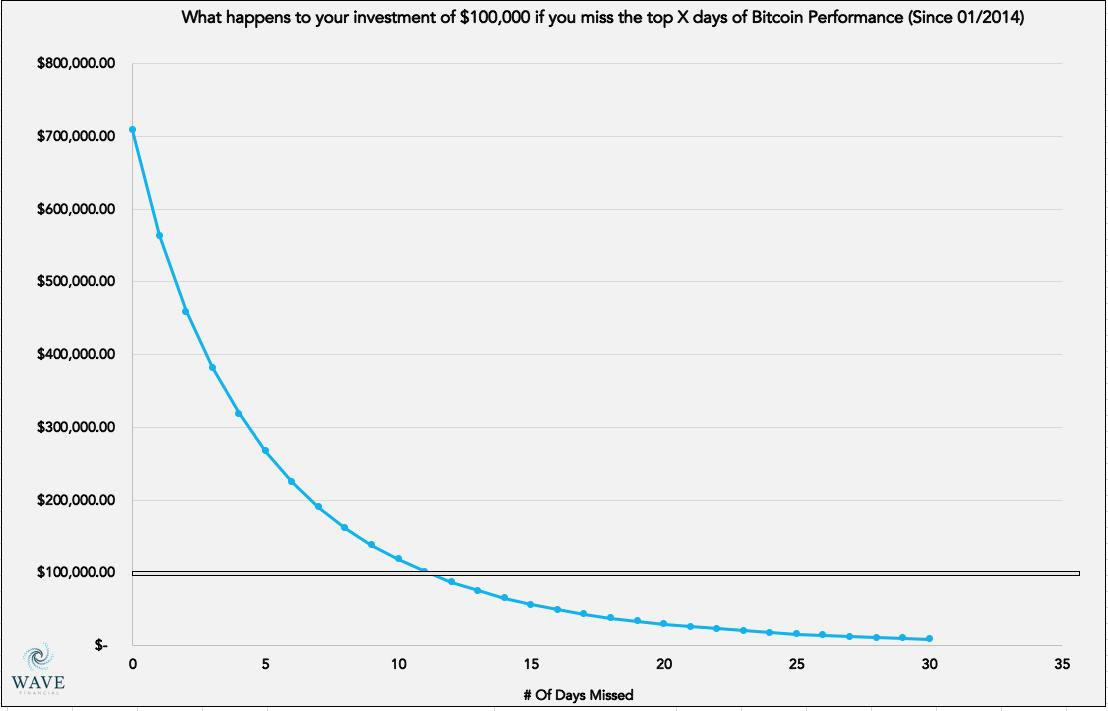

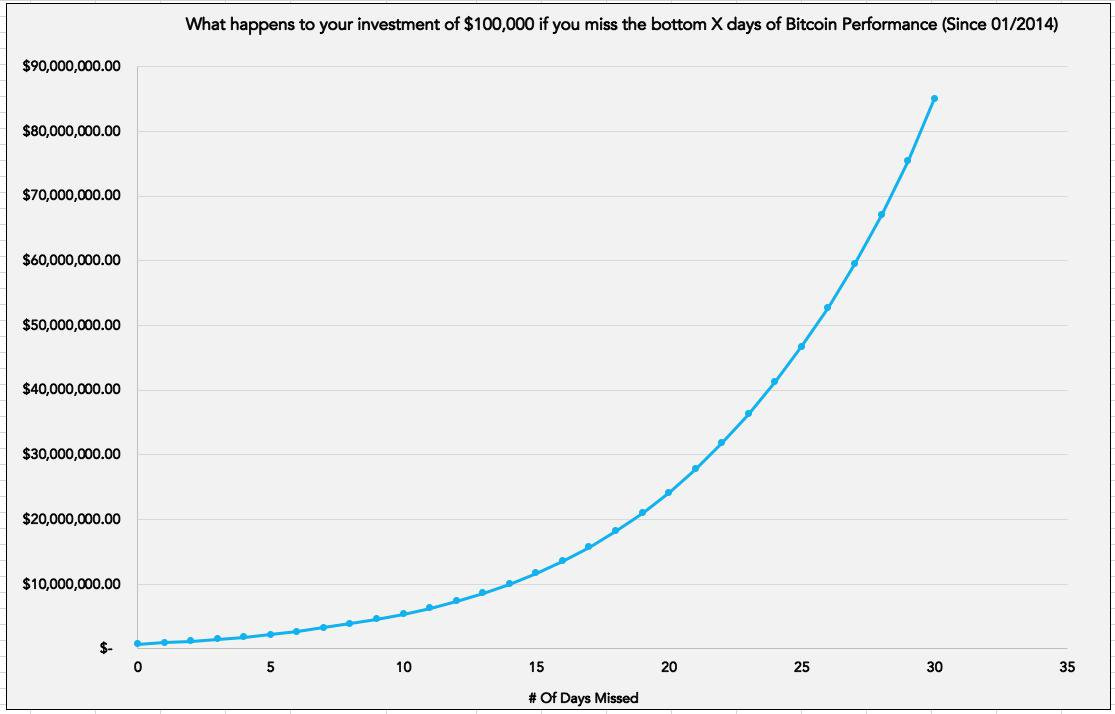

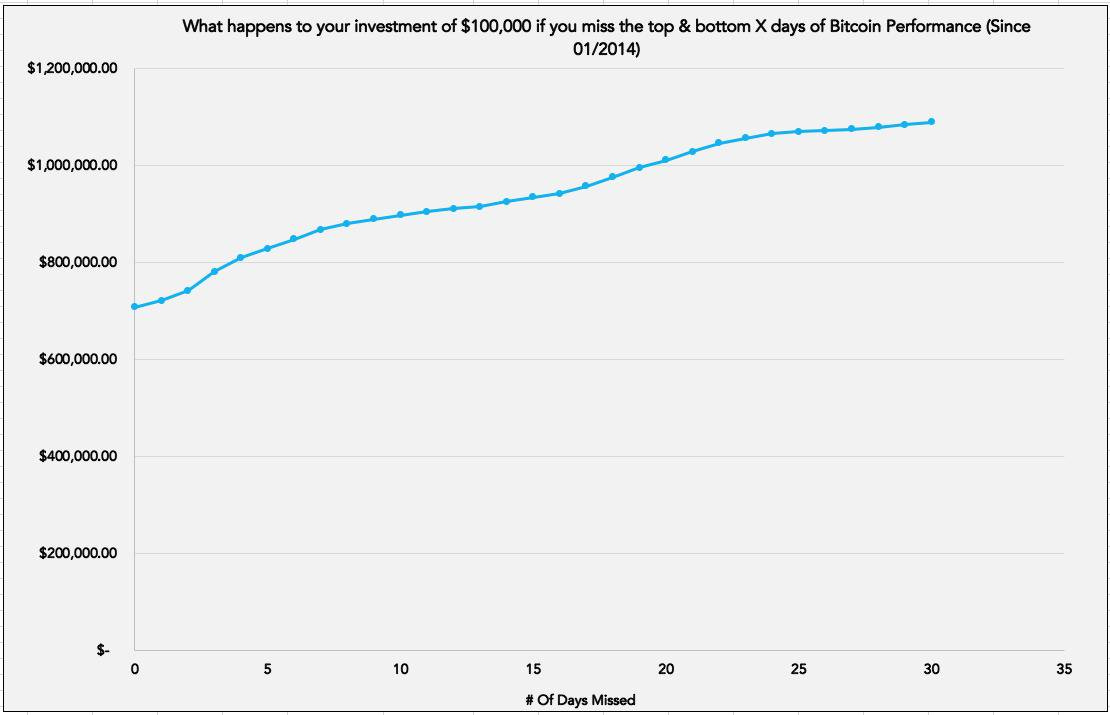

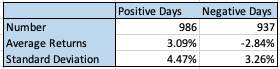

The return profile of Bitcoin is an interesting topic to dive into, and I wanted to share a few data points I found particularly interest (I’ve tweeted some of these before).

Basically, Bitcoin posts mosts of its gains and losses in a minority of days (highly bi-model returns — something to keep in mind when pricing options because naive Black-Scholes assumes normal distribution)

This return profile also means that volatility and implied volatility often rise as Bitcoin rises (which is NOT the case in the traditional markets — volatility falls off during bull markets)

As you can see, volatility is on the rise along with price. Going short calls in a Bitcoin bull is much more dangerous than shorting calls in an equities rally.

Join the conversation on Telegram and Twitter

If you ❤️ our newsletter, tell your friends about us!

Nothing written in CryptoAM is legal or investment advice and should not be taken as such. CryptoAM does not make any guarantee or other promise as to any results that may be obtained from using our content. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence.