CryptoAM: Initial Exchange Offerings, Blockchain Lobbyists, and Interest Accounts

Hey CryptoAM team. We wanted to welcome those of you who aren’t already in to our Telegram group. Fire conversation, punting altcoins and vaporwave memers are welcome.

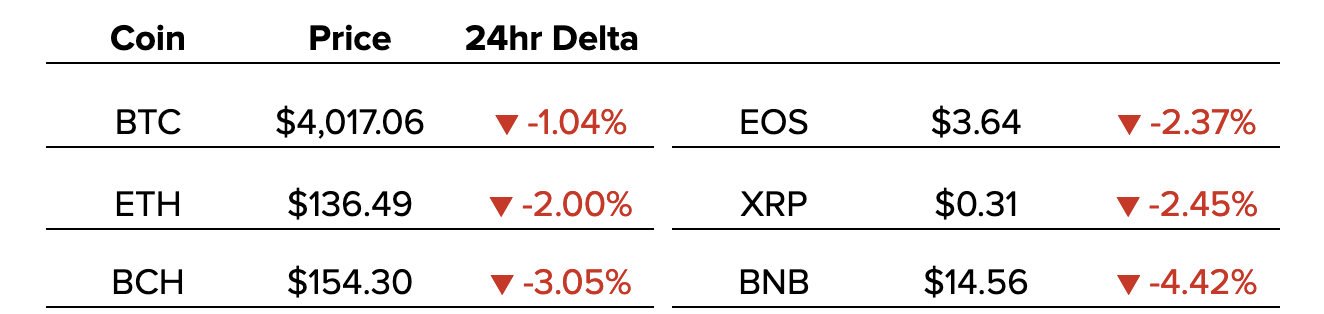

3 things you need to know:

One: IEO is the new ICO?

Here’s a funny story. This new hot thing suddenly becomes illegal. So someone invents a slightly different version of that hot thing, and then offers that hot thing to the world?

Not so funny actually. But, effective! That’s whats happening with these so called “initial exchange offerings” which is just a different and splashier way of getting listed on a major exchange. Binance introduced this idea earlier this year with the formation of Binance Launchpad.

So, what is an IEO exactly?

An Initial Exchange Offering (IEO) relies on having an exchange (or set of exchanges) function as the counter-party. Developers mint the project’s tokens and send them to the exchange, which will then sell the tokens to individual contributors for Ether. Subject to the agreement between the developers and the exchange, conditions traditionally found in an ICO can be emplaced in an IEO. These conditions include capping the contribution per individual and having a fixed price per token.

From the perspective of a contributor, instead of sending Ether to a Smart Contract governing the ICO, each IEO participant has to create an account with the exchange and send ETH to this account. When the IEO commences, the participant can purchase the token directly from the exchange.

Since the original Binance announcement many exchanges have indicated their intention to have their own versions of IEOs.

Already announced include:

Huobi

Bitmax

KuCoin

I would expect more to be coming soon, as this is actually a great deal for both tokens and exchanges. Exchanges get a cut (usually 10%) of the tokens, and tokens get access to an eager market, ready to drive up the price of their token. The key will be getting access to high quality tokens and getting access to high quality buyers — which indicates to me the smaller exchanges are going to have a tough time.

Two: Blockchain lobbying efforts triple in DC

Entities lobbying on blockchain related issues increased from 12 to 33 from 2017-2018, according to Politico.

The majority of this lobbying spend goes towards shaping securities laws. This kind of lobbying can be retroactive or proactive: Projects that have already been launched want to ensure that they don’t face future regulatory action if their launch may have broken securities laws at some point. Other lobbying may be to shape future laws so that there is clear regulatory clarity for future projects and token sales.

Why you should fight against your libertarian impulses: We’ve written recently about the superstar status of the SEC and their commissioners in the crypto space. But the SEC only enforces existing securities laws, Congress is the one who actually helps shape them. If Congress were to grant clear exemptions to securities laws for cryptocurrencies that met certain requirements, as we saw recently in Colorado, then this would be a game changer for the blockchain industry in the US.

The big picture: Securities law reform will take time and so the SEC will continue to be a major player in the US Crypto space for the foreseeable future. The key bill to watch going through Congress is the Token Taxonomy Act, which clearly defines digital tokens and when they are not securities.

Blockchain lobbyists 101 of who matters in town: Kristin McKenzie Smith of The Blockchain Association, Jerry Brito of Coin Center, and Perianne Boring of The Chamber of Digital Commerce. Politicos leading the charge in favor of the industry include Darren Soto and David Schweikert of the Blockchain Congressional Caucus.

P.S. Totally unverified comment from a friend working on the Hill - Ripple has the strongest lobbyist presence in town which makes sense, given they have the most to lose from potential regulatory action…

Three: BlockFi Savings Account Attract Significant Interest

BlockFi announced yesterday that it had attracted more than $35 million in crypto and 10,000 customers for their interest-yielding deposit accounts, with $25 million in the last two weeks alone. This follows their announcement earlier this month that they would offer deposit accounts yielding 6.2% interest on Bitcoin and Ethereum deposits.

BlockFi isn’t making money on this. In fact it’s a loss leader, according to BlockFi CEO Zac Prince. He went on to explain:

“This product will be for some amount of time, probably for 3 to 18 months…”

BlockFi can change this interest rate as they please. While 6.2% is an unbelievable rate, this is unlikely to be an offering that lasts over the long run. Also as we explained in an earlier edition, funds deposited in BlockFi’s accounts aren’t covered by Federal Deposit Insurance. That means that if BlockFi goes bankrupt, account holders could lose up to 100% of their savings unlike in traditional fiat deposit accounts.

Expect to see more of this from BlockFi. They’ve already announced their intention to introduce a new product every six months as they look to rapidly increase their user base. The reason why they can afford to this is because they’re heavily venture backed, including a $52.2 million round in July 2018.

Our thought bubble: Passive income in cryptocurrency has become a hot topic. Prediction: All the loan platforms, staking platforms, etc. that are discussing passive income will have a hard time in a bull market just as exchanges did in the bear market. Even 100% APR wouldn't stop someone from punting altcoins.

Also in the news:

Market Outlook:

Quick Take

Direction: This is natural profit taking, and the pullback that we expected on Tuesday. Fundamentals are slowly shifting positive, as are many major indicators. As long as we hold above the bottom of the red area outlined (3850) we are still likely to trend upwards in my opinion.

Key Support: 3910, 3850

Key Resistance: 4040, 4100

Overall Market: We’ve seen select altcoins begin to pop off, while BTC trends upwards or mostly flat.

In early 2017, we saw Ethereum lead the market forward and then saw its gains spill over to altcoins and fuel the meteoric rise. I’d expect much of the same to fuel the next bull run, and will be looking for specific milestones that will inform how to construct the more lucrative portfolio. I’d expect a similar run by a 2nd tier protocol to lead the market before we can officially call a bull market. This protocol in my opinion is likely to be one (or more) of the following: Binance Chain, Holochain, Tezos, EOS, Dfinity, Cardano, or BAT (despite not being a protocol - feel free to ask in our telegram chat why).

The end of the bear markets have tended to look like the following:

High caps -> mid caps -> small caps. I’d assume Bitcoin will lead the charge, and bring back some semblance of hope to the markets. Once you see correlations begin to unwind combined with an upward trend, it is likely an EV positive play to enter into some long BTC positions. Once BTC breaks above 6k, it’s more likely the steam will begin to pick up in a large way.

As a note, the altcoins gains you are seeing here are due to BTC losing volatility and speculators pouring. Proportionally the alt market is gaining against BTC despite the overall market-cap remaining flat, suggesting that this is just the sloshing around of speculative capital trying to catch gains rather than new capital inflows (needed for a true bull run).

One confounding factor here is the introduction of new fiat portals which may lead to alts with fiat entries rising sharply with Bitcoin before spilling to the rest of the market.

What I’m thinking today:

Exploring Crypto-assets and Central Banks

I’d like to take a moment to dig into where cryptocurrencies fit into society overall, and what the drivers of growth and implications of success might look like. These are complicated questions and will not be answered in full (or maybe even at all) here, but hopefully the resources, materials and discussion below will help frame the journey.

I want to make the distinction between something like Bitcoin (a cryptocurrency) and something like Ethereum (a crypto-network). This may seem like a trivial distinction but it’s important for the following discussion because cryptocurrencies and crypto-networks have very different uses.

I believe it’s best to start with the large scale question of “how does our current financial system operate and then dive into the next question of “where do cryptocurrencies fit.”

The first question is relatively simple. Countries issue currencies, and generally a central bank will attempt to manage the inflation and interest rates of said currency in order to create economic stability. The issuance of a cryptocurrency attempts to circumvent two institutions, the money issuer (Dept. of Treasury in the U.S) and the money manager (the Federal Reserve).

As currencies work today, if you search “central bank” and cryptocurrencies, you’ll come across a variety of different takes but by far the most common are (1) cryptocurrencies are a threat to central banks and (2) central banks will issue their own cryptocurrencies.

With respect to (1), there are a variety of reasons why cryptocurrencies could be disruptive to traditional financial systems:

Return to commodity based money from the credit based system we use today

Faster settlement for large amounts of capital

More divisibility, micropayment enabled

Insulated from currency mismanagement (seen in many countries)

Same level of anonymity as cash

There are also risks:

Deflationary risk

Software risk

Non-management risk (If no one controls it — can anyone fix it?)

If cryptocurrencies became more widely accepted, it would likely be driven by mistrust in our current institutions to upkeep both infrastructure and manage our economies. This would likely displace central banks, but I do not think it would replace traditional banks at all. What would be the most likely outcome is a similar banking system, but with a unit of account that is Bitcoin instead of the dollar, similar to countries that use the dollar as a unit of account despite having a local currency.

With respect to (2), it’s unlikely a central bank would issue a digital currency in a country with a robust financial system, as that currency would eat deposits from banks, reducing lending and reducing consumption, leading to lower growth rates.

Further reading:

Join the conversation on Telegram and Twitter

If you ❤️ our newsletter, tell your friends about us!

Nothing written in CryptoAM is legal, or investment advice and should not be taken as such. CryptoAM does not make any guarantee or other promise as to any results that may be obtained from using our content. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence.