CryptoAM: Central Banks, Bitcoin Rebounds & Microsoft Enters

“If I’d only followed CNBC’s advice, I’d have a million dollars today. Provided I’d started with a hundred million dollars.” - Jon Stewart

Three things you need to know:

One: Coinbase* looks to acquire Xapo

Coinbase’s quest to diversify its revenues continues. The exchange is reportedly close to buying Xapo, one of the most prominent custody businesses in the industry, for $50 million. If successful, it would be the 15th acquisition Coinbase has made since its inception.

Xapo is one of the largest custodians in the industry, with around 700,000 BTC worth of assets under custody, representing close to $5.5 billion. Coinbase already offers custody services but has only $1 billion under custody, meaning that the proposed acquisition would significantly boost Coinbase’s share in the custody market. Other well known custodians in the industry are BitGo and Kingdom Trust.

Key trend: As the industry matures and more institutions enter, look for custody to increase in importance. No institution wants to run the risk of losing their funds, and this industry is rife with examples of hacks and lost private keys. High quality custody solutions give confidence to institutions that their funds will be kept safe, encouraging them to enter and increase their exposure. I also expect the further consolidation of the cryptocurrency industry. There is far too much fragmentation across all the different sectors. Exchanges, custodians, protocols, dApps, and payment rails are all incredibly fragmented and it’s odd to see an industry focused on the renewal of the financial system to have so many silos. If I were making bets (and I am), I would bet on the streamlining of many different offerings that are doing tangentially related things.

Be smart: Back in 2014 Xapo raised $40 million from investors in what was, at the time, the largest investment in a crypto company. Without knowing the term sheets or specifics, being sold for $50 million after raising $40 million doesn’t appear on the surface to be a great outcome for those initial investors…

Two: Flexa + Gemini = using crypto at Whole Foods

If you’ve spent any amount of time in this industry I’m sure you’ve heard a critique resembling the following:

“You can’t use crypto for anything outside of trading”

“Crypto can’t be true money because it’s not a true medium of exchange”

“If this is money why can’t I buy coffee with it?”

It’s a fair criticism, because most mainstream retailers don’t accept crypto. Not only that, but during the fee crisis of late 2017, many retailers that previously supported Bitcoin actually rescinded that support citing unstable payments.

General reasons for this lack of adoption include low demand, complicated accounting, and technical difficulties integrating crypto into traditional payment infrastructure. There have been a few attempts to mitigate this from companies such as Bitpay and Coinbase custody, but the vast majority of Bitcoin payments are still confined to grey & black markets (which are forced to use Bitcoin since they can’t really accept anything else).

That’s why last week’s announcement from Flexa, the payment processor, has received mainstream attention. The company claims you can use their mobile wallet, named SPEDN, to purchase goods at major retailers such as Whole Foods, Bed Bath and Beyond, and Nordstrom.

The secret sauce behind all of this? These retailers aren’t actually touching crypto!

Our Bitcoin hero Blake puts crypto on his SPEDN wallet (currently can hold Bitcoin, Ether, Bitcoin Cash, and Gemini Dollar).

Blake goes to buy groceries from Whole Foods. He opens up his SPEDN wallet, chooses which currency to use, and then scans the uniquely generated QR code on his wallet with the store’s digital scanners (no new infrastructure required for the store).

The Flexa backend converts Blake’s crypto into fiat and makes the payment to the retailer. The retailer never touches crypto, and instead just sees a successful transaction on their screens, immediately. This experience can best be compared to AliPay or WeChat, except users are obviously paying with crypto. Flexa acts as an intermediary taking on the currency risk at the time to allow you the ability to pay with your Bitcoin.

What about block confirmation time? Flexa gets around this by requiring that SPEDN stake a certain amount of the company’s native Flexacoin on the network. This serves as collateral to settle the transaction. While block confirmations take place, the merchant is compensated in real time.

The overall vision for Flexa: Imagine your major wallet providers plugging into the Flexa network, allowing all their users to access the large retailers that Flexa has. For example if I was using Trust Wallet and it was signed up to the Flexa network, I would also be able to purchase goods at Whole Foods. The more providers that use the Flexa network the more demand there is for Flexacoin, potentially pushing up the price over time.

Why this matters: Mainstream adoption of crypto requires mainstream retailers to accept it, allowing people to buy their regular goods and services.

What I’ll be watching for: Continued partnerships with big brand retailers, transaction volume on the network, and how many active users there are. This is a great opportunity for stablecoins, and so I’ll be watching to see if there is a significant increase in demand for Gemini Dollar.

Oh, and I’ll be waiting for an Android app also (as if getting left off group chats wasn’t already bad enough).

Three: Microsoft launches testnet for decentralized identity network

Microsoft announced last week that it was previewing a new network called ION (Identity Overlay Network), on top of the Bitcoin blockchain. ION is a decentralized identifier network, which allows users to establish their identities without needing to go through a central party.

ION is the first implementation of what Microsoft calls Sidetree. This is a protocol that enables decentralized identifier networks to be built on top of blockchains. This is important because it solves scalability issues that blockchains currently face, meaning that most can’t handle more than tens of transactions per second.

Why is digital identity important? Because it allows us to authenticate who we are so that we can access services on the internet. Every time you give your email and password, you are giving proof of who you are and that you are the person behind an account.

The problem currently is that having identity centralized exposes the system to leaks, hacks, and general invasions of privacy. You don’t want your account information, details, and personal information to fall into the hands of bad actors.

The best way to think about centralized identity is to take Facebook Connect as an example. When you move across various sites on the internet you often see two options:

Sign up for an account

Sign in via Facebook

If you sign in via Facebook, then Facebook pushes the data that it already has on you to that website, to automatically verify your identity and create and account.

Ideally with decentralized identity you the individual should have your own personal version of Facebook Connect, allowing you to navigate and access applications. This would happen while having full control over your personal details. The specific details you would need to provide to applications to authenticate your identity are still being considered, with industry players banding under the Decentralized Identity Foundation to help answer provide solutions.

Not only does decentralized identity increase privacy and reduce the risk of leaked data, but it can help lay the backbone for millions of people in developing countries without a formal identity to access financial and governmental services.

Microsoft is currently running ION on the Bitcoin testnet, with the mainnet launch scheduled for the coming months.

Read the original Microsoft announcement here and read more on digital identity.

One Extra thing: Bitcoin ETF gets Delayed (again)

The first time that a Bitcoin ETF got denied / delayed the market took a walloping. The second time the beating wasless. By now, the market seems immune to bad news about an ETF.

If you’re holding out hope for an ETF approval, I’d bury that hope pretty quickly. The SEC has been denying and delaying different Bitcoin ETFs for over 2 years now. Seeing as they delayed this application once again, it’s unlikely it gets approved anytime soon. The market will have to mature dramatically before an ETF will be approved.

Perhaps one good way to play the probability of an ETF approval is to consider it a black swan, and take the Nassem Taleb approach. Make a lot of tiny bets that mostly lose and wait for the swan to hit to cover all the times you’ve lost.

Structurally, that looks like taking out extra leverage a few days around decision time and eating the losses until you win big.

Of course…who knows. Maybe the SEC will announce at a random time just to mess with us.

Also in the news:

Market Outlook:

Quick Take

Overall Market: Some interesting developments over the past week. We’re seeing strong dips get bought up quickly, in an inversion of the 2018 dynamic the market experienced. This to me indicates we are indeed in the fourth Bitcoin bull, and one should navigate the market accordingly.

I’d like to note before moving on that *despite* being in a bull run there will be significant pull backs. Every run has seen 30%+ pull backs. When I say bull run, I mean that I expect it’s incredibly likely the price of Bitcoin will end 2019 above where it is today.

The crash from 8000 — > 6800 last week was likely caused by panic selling after a large $31M order on Bitstamp was sold at market. In my opinion this was a clear case of market manipulation. It’s not a coincidence the Bitcoin was sold on the most illiquid BitMEX reference rate exchange. Around $250M worth of longs were liquidated in the move, further exacerbating the crash.

The overall market acted rationally by quickly buying up the dip.

We’re now seeing strong action from altcoins, with Bitcoin dominance falling as Bitcoin ranges between 7800 - 8000 (as expected, alts post gains after BTC cools off).

As for the reasoning behind the continued price action, there are a few reasons that make sense:

There are growing trade war concerns with China & the fall of the CNY vs USD leading to capital flight via Bitcoin.

There is also increased public & institutional awareness of Bitcoin, and better infrastructure, so that people on the sidelines can enter the market. Google trends & media coverage has grown significantly since the beginning of the year.

At the beginning of 2019 there were many underweight crypto hedge funds with sidelined capital. They could not risk Bitcoin taking off without them as they understand that Bitcoin posts the majority of its gains in a small amount of days, meaning that missing those days would leave them in the dust compared to their benchmark.

Institutional short exposure to BTC. There are now a variety of regulated ways to go short BTC, which also means more violent moves on the way up as shorts get quickly unwound.

Some notes:

We are seeing the return of alt season, led by Binance launchpad coins. If you aren’t trying to get into the Harmony launchpad sale, you may want to reconsider. It’s getting offered at 1/2 the price of the seed sale, a first. Binance seems to offer launchpad coins at a steep discount to ensure a nice return on listing.

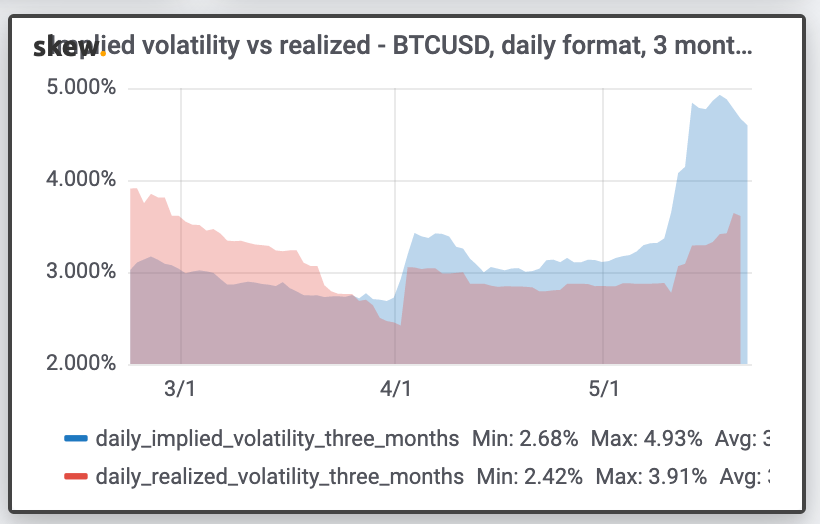

Implied volatility has spiked massively on Deribit, leaving a wide gap between realized vol. This had led me to begin selling short term vol. Have short positions on the following contracts: MAY24- 7250P, MAY24- 7500P, MAY24- 8500C, MAY24-8750C, MAY31-8750C, MAY31- 7250P.

Implied vol is forward looking, realized vol is backwards looking. It’s not a perfect comparison but when there is a wide and continued gulf between the two the market may be mispricing.

Direction: We are currently in a bullish continuation pattern but have failed the first breakout. A break above 8100 should sent us to the 8400 level quickly, and a break below 7720 would likely send us down the 7400 level. I’m net long, and believe that Bitcoin is more likely to test 8400 first than 7400.

I’m very overweight in altcoins right now, and am actively entering into positions in coins that:

Have strong bottoming patterns

Large asian markets

Strong communities

Protocol or Currency, not dApp

Key Support: 7720, 7400

Key Resistance: 8100, 8400