CryptoAM: Banking woes, Tezos glows & Facebook grows

☀️It’s Thursday morning here in Los Angeles, and the sun is finally coming out after a weeks worth of East Coast weather!

Three things you need to know:

One: The crypto banking crisis

The traditional banking system is failing cryptocurrency companies. If you’ve worked in crypto, you’re familiar with the trials and tribulations of getting a bank account, running payroll and generally keeping your company afloat. You’ve heard these words before:

High risk

KYC/AML

Security concern

In the U.S. there are the least some banks such as Metropolitan & Silvergate that take on cryptocurrency companies. According to the Block, these options don’t exist in Europe.

Here’s an absolutely hilarious part of the piece:

“You have to either go with a crappy bank or slip through the cracks,” the crypto hedge fund manager tells The Block, saying he chose the latter route via a bespoke U.S. bank after a 9-month endeavor.

Other sources say Barclays bank has “one guy” who can help crypto firms “slip through,” but the bank is not publicly accepting of crypto applications. The source would not disclose the name of the Barclays employee, calling him a “trade secret.”

Seriously! There’s one guy, whose name I assume is Fernando, that knows how to work the system. Does he tell his coworkers? Who knows! Maybe Barclays has blessed him, the poor sacrificial lamb. Oh no, Fernando opened a ton of accounts for crypto companies — have to let him go. We totally had no idea.

Anyway, this is actually a real pain point that has plagued the industry since day one, due to the high security concerns that many have about the cryptocurrency world.

Fun fact, my uncle tried to start a credit union in 2015 that got shut down by the Feds because they were accepting Bitcoin companies. Such is the way the tumbleweed goes.

Why this matters: Despite the fact that “being your own bank” is a central to the idea of cryptocurrency, it’s not a reasonable task in this world. In order to succeed and thrive, you need to be able to access and use traditional infrastructure. It’s the only way the world runs. Jurisdictions (like the EU) that restrict the operational ability of cryptocurrency companies will soon find themselves missing innovation and progress. The beauty of running a company in the cryptocurrency space is the ability to relocate and re-establish wherever you go. After all, it’s all online.

Go deeper: Read the full article

Two: Tezos passes its first on-chain blockchain update

Source: Cryptonewz.com

Tezos, the 16th ranked cryptocurrency with a market size of over $1 billion, successfully self-amended itself for the first time via its on-chain governance procedure with the activation of the Athens A proposal.

Tezos runs on a consensus mechanism called Liquid Proof of Stake. The Athens A proposal achieved two key outcomes:

Reduced the minimum amount needed to stake on the network by 20%. This makes it easier for smaller Tezos holders to participate in validating transactions.

Increased computation limits on blocks. This means that larger transactions can be run through the Tezos blockchain.

What’s unique about this: Usually with upgrades to blockchains, like the Constantinople upgrade to Ethereum earlier this year, users who run nodes on the network have to manually upgrade them to fit with new updates.

In the Tezos network however updates that pass through on-chain governance are automatically pushed to all nodes at a specified block number. The key quote, as per an interview with Jacob Arluck on Coindesk:

“…instead of everyone updating their software, the upgrade gets pushed to everyone’s computers.”

The big trend: The Athens update is part of a larger turnout for Tezos. Up until recently the project was better known for its internal governance turmoil, with a court case brought against the chairman of the Tezos foundation - by two of its co-founders no less.

What I’m thinking: Blockchain governance can be a controversial topic, and oftentimes feels theoretical and difficult to understand. I found this post here very enlightening regarding the Tezos process and comparisons with other governance systems like MakerDAO and Aragon.

Spoiler alert: The Tezos community comes off as far more engaged than MakerDAO and Aragon, both in terms of total number of participants and the total % of XTZ (Tezos token) that is staked in governance decisions.

Three: Study - Facebook would bring new users to crypto

Source: Blokt

Are you tired of hearing news about Facebook’s massively hyped entrance to crypto?

Tough. Because it matters and here’s another interesting reason why (it could benefit you financially if that helps).

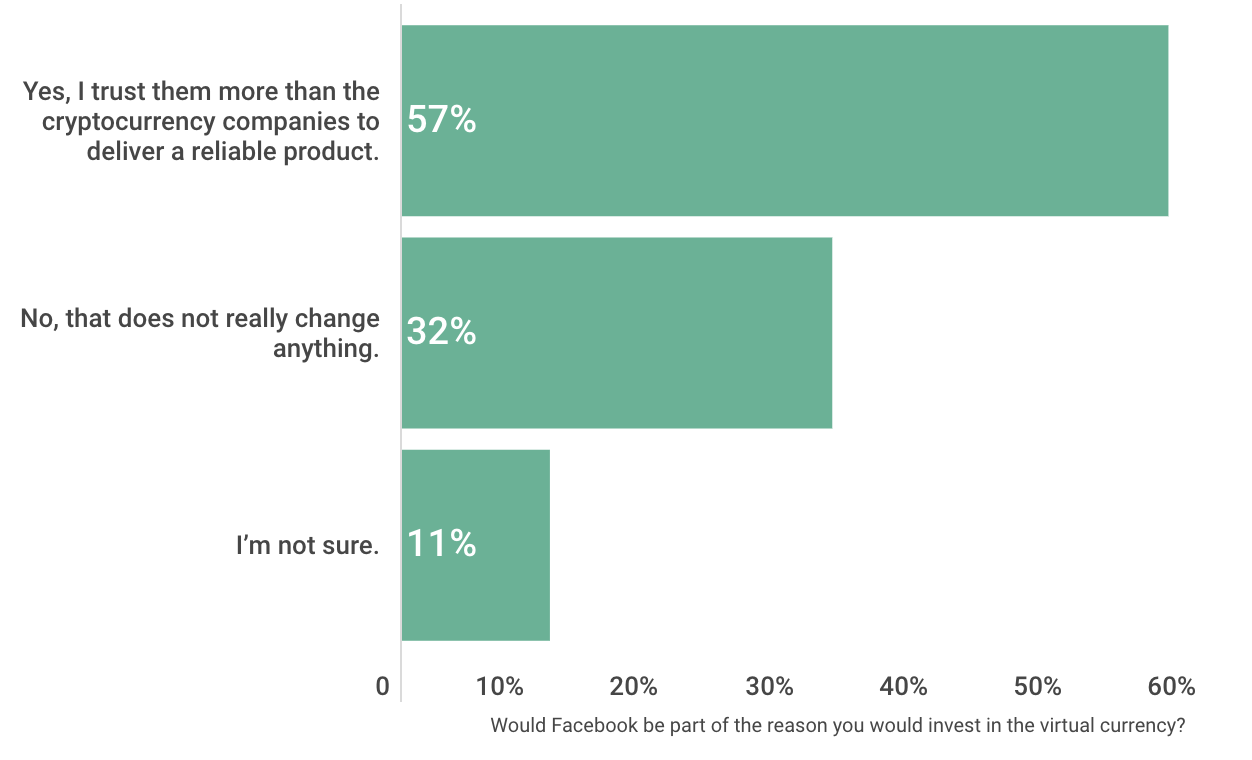

Financial information site LendEDU surveyed 1,000 Americans, here’s the run-down on the most interesting parts of the results:

7% of respondents have already invested in crypto at some stage

18% of total responders would invest in a Facebook created cryptocurrency

57% of people who said they would invest in Facebook Coin would do so because they “trust them more than the cryptocurrency companies to invest to deliver a reliable product.”

Source: LendEdu.com

Let’s start with a bit of gentle teasing. Most reports point to Facebook’s crypto being something resembling a stablecoin. Those that really take a ‘risk’ then and ‘invest’ in Facebook coin might be disappointed when they find their investment doesn’t turn them into lambo drivers but instead ends up being a nice wee store of value for them.

On a serious note. One way to interpret the study is to say that the amount of people holding at least one crypto could more than double with the introduction of Facebook Coin. And you can bet that at least a portion of people who get on-boarded to crypto via Facebook Coin would venture out to buy other cryptos once they get comfortable with the idea of buying and selling cryptocurrency.

Also in the news:

Market Outlook:

Quick Take

Direction: These last few days have seen absolutely wild price action. I’ve flipped to lean bearish based on the incredibly strong rejection of 9000. It seems like the bulls are getting exhausted. The volumes on the selloff matched the volume on the run from 8000 —> 8600.

Strong rejections & wicks mean that there are not enough people buying over the rejected level. This indicates to buyers at lower levels that the higher prices they are betting on are unsustainable and they revise their buys downward. You can draw two things from this:

The longer we stay at previous levels, the more likely it is for bullish continuation as people start to believe prices are justified. For example, if we’re at 8600 in a week, I’d flip to bull.

The drop will be quick if so, as buyers will panic on the way down and clear out their orders from the books. We’ll probably see long wicks to the downside.

I’m expecting us to revisit 8200, which would be an ideal buy zone. I’ll be entering into positions in the 8200-8300 range. If we break below 8200 I think 7800 is the next likely target.

Key Support: 8230

Key Resistance: 8710

What I’m thinking today:

One of the most enduring questions in the crypto-space concerns the role of Bitcoin in the world. Since its creation in 2008, people have argued over what exactly bitcoin is. Is it for cheap payments? Is it a store of value? Is it for privacy?

Over time, our definitions of what Bitcoin should be used for have changed. I’ve included an excerpt here from Nic Carter’s great article, where he goes over what the 7 main definitions of Bitcoin are, and how they have changed over time.

E-cash proof of concept: the first major narrative, this was the general view of Bitcoin in its earliest days. Back then, cypherpunks and cryptographers were still appraising the nascent project and determining whether it worked, if at all. Since all prior e-cash schemes had failed, it took a while for people to be convinced of its technical and economic viability and move on to more expansive conceptions of the protocol.

Cheap p2p payments network: an extremely popular and pervasive narrative. Some believe this is what Satoshi had in mind — a straightforward currency for peer to peer internet transactions. A decentralized Paypal or Venmo, if you will. Since microtransactions are a key component of internet commerce, proponents of this view generally believe that low fees and convenience are an essential characteristic of such a currency.

Censorship-resistant digital gold: the counterpoint to the p2p payments narrative, this is the view that Bitcoin primarily represents an untamperable, uninflatable, largely unseizable, intergenerational wealth store which cannot be interfered with by banks or the State. Proponents of this view de-emphasize Bitcoin’s use for everyday transactions, arguing that security, predictability, and conservatism in development are more important. We’re callously lumping in sound money believers into this camp.

Private and anonymous darknet currency: the view that Bitcoin is useful for anonymous online transactions, in particular to facilitate black market online commerce. This is not necessarily mutually exclusive with the e-gold position, as many proponents of the digital gold view believe that fungibility and privacy are important attributes. This was a popular narrative before the chain analysis companies had success de-anonymizing Bitcoin users.

Reserve currency for the cryptocurrency industry: this is the view that Bitcoin serves an essential purpose as the native currency for the cryptocurrency/cryptoasset industry more generally. This is a view espoused by traders for whom BTC is the numeraire — the currency in which the prices of other assets are quoted. Additionally, traders, businesses, and distributed networks that hold reserves in BTC de-facto endorse this view.

Programmable shared database: this is a slightly more niche view, and generally involves the understanding that Bitcoin can embed arbitrary data, not just currency transactions. Individuals holding this view tend to see Bitcoin as a programmable, expressive protocol, which can facilitate broader use-cases. In 2015–16, it was popular to express the notion that Bitcoin would eventually absorb a diverse set of functionalities through sidechains. Projects like Namecoin, Blockstack, DeOS, Rootstock, and some of the timestamping services rely on this view of the protocol.

Uncorrelated financial asset: this is a view of Bitcoin that treats it strictly like a financial asset and finds its most important feature to be its return distribution. In particular, its tendency to have a low or nonexistent correlation to all manner of indexes, currencies, or commodities makes it an attractive portfolio diversifier. Proponents of the view are generally not too concerned about owning spot Bitcoin; they are interested in exposure to the asset. Put another way, they want to buy Bitcoin-flavored risk, not necessarily Bitcoin itself. As Bitcoin has become more financialized, this conception has gained steam.

Join the conversation on Telegram and Twitter

If you ❤️ our newsletter, tell your friends about us!

Nothing written in CryptoAM is legal or investment advice and should not be taken as such. CryptoAM does not make any guarantee or other promise as to any results that may be obtained from using our content. No one should make any investment decision without first consulting his or her own financial advisor and conducting his or her own research and due diligence.